CORONAVIRUS EMERGENCY LOANS SMALL BUSINESS GUIDE AND CHECKLIST

The Coronavirus Aid, Relief, and Economic Security (CARES) Act allocated $350 billion to help small businesses keep workers employed amid the pandemic and economic downturn. Known as the Paycheck Protection Program, the initiative provides 100% federally guaranteed loans to small businesses.

Importantly, these loans may be forgiven if borrowers maintain their payrolls during the crisis or restore their payrolls afterward.

The administration soon will release more details including the list of lenders offering loans under the program. In the meantime, the U.S. Chamber of Commerce has issued this guide to help small businesses and self-employed individuals prepare to file for a loan.

Here are the questions you may be asking and what you need to know.

-

Am I ELIGIBLE?

You are eligible if you are:

- A small business with fewer than 500 employees

- A small business that otherwise meets the SBA’s size standard

- A 501(c)(3) with fewer than 500 employees

- An individual who operates as a sole proprietor

- An individual who operates as an independent contractor

- An individual who is self-employed who regularly carries on any trade or business

- A Tribal business concern that meets the SBA size standard

- A 501(c)(19) Veterans Organization that meets the SBA size standard

In addition, some special rules may make you eligible:

- If you are in the accommodation and food services sector (NAICS 72), the 500-employee rule is applied on a per physical location basis

- If you are operating as a franchise or receive financial assistance from an approved Small Business Investment Company the normal affiliation rules do not apply

REMEMBER: The 500-employee threshold includes all employees: full-time, part-time, and any other status.

-

What will lenders be

LOOKING FOR?

In evaluating eligibility, lenders are directed to consider whether the borrower was in operation before February 15, 2020 and had employees for whom they paid salaries and payroll taxes or paid independent contractors.

Lenders will also ask you for a good faith certification that:

- The uncertainty of current economic conditions makes the loan request necessary to support ongoing operations

- The borrower will use the loan proceeds to retain workers and maintain payroll or make mortgage, lease, and utility payments

- Borrower does not have an application pending for a loan duplicative of the purpose and amounts applied for here

- From Feb. 15, 2020 to Dec. 31, 2020, the borrower has not received a loan duplicative of the purpose and amounts applied for here (Note: There is an opportunity to fold emergency loans made between Jan. 31, 2020 and the date this loan program becomes available into a new loan)

If you are an independent contractor, sole proprietor, or self-employed individual, lenders will also be looking for certain documents (final requirements will be announced by the government) such as payroll tax filings, Forms 1099-MISC, and income and expenses from the sole proprietorship.

-

How much can I BORROW?

Loans can be up to 2.5 x the borrower’s average monthly payroll costs, not to exceed $10 million.

How do I calculate my average monthly PAYROLL COSTS?

INCLUDED Payroll Cost:

- For Employers: The sum of payments of any compensation with respect to employees that is a:

- salary, wage, commission, or similar compensation;

- payment of cash tip or equivalent;

- payment for vacation, parental, family, medical, or sick leave

- allowance for dismissal or separation

- payment required for the provisions of group health care benefits, including insurance premiums

- payment of any retirement benefit

- payment of state or local tax assessed on the compensation of the employee

- For Sole Proprietors, Independent Contractors, and Self-Employed Individuals: The sum of payments of any compensation to or income of a sole proprietor or independent contractor that is a wage, commission, income, net earnings from self-employment, or similar compensation and that is in an amount that is not more than $100,000 in one year, as pro-rated for the covered period.

EXCLUDED Payroll Cost:

- Compensation of an individual employee in excess of an annual salary of $100,000, as prorated for the period February 15, to June 30, 2020

- Payroll taxes, railroad retirement taxes, and income taxes

- Any compensation of an employee whose principal place of residence is outside of the United States

- Qualified sick leave wages for which a credit is allowed under section 7001 of the Families First Coronavirus Response Act (Public Law 116– 5 127); or qualified family leave wages for which a credit is allowed under section 7003 of the Families First Coronavirus Response Act.

-

Will this loan be FORGIVEN?

Borrowers are eligible to have their loans forgiven.

How Much?

A borrower is eligible for loan forgiveness equal to the amount the borrower spent on the following items during the 8-week period beginning on the date of the origination of the loan:

- Payroll costs (using the same definition of payroll costs used to determine loan eligibility)

- Interest on the mortgage obligation incurred in the ordinary course of business

- Rent on a leasing agreement

- Payments on utilities (electricity, gas, water, transportation, telephone, or internet)

- For borrowers with tipped employees, additional wages paid to those employees

The loan forgiveness cannot exceed the principal.

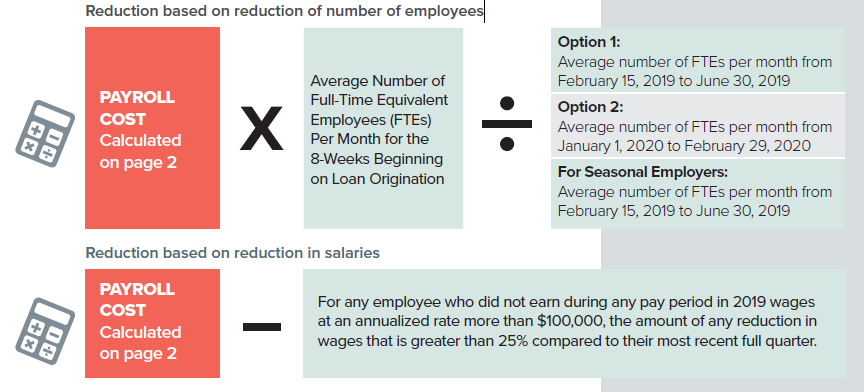

How could the forgiveness be reduced?

The amount of loan forgiveness calculated above is reduced if there is a reduction in the number of employees or a reduction of greater than 25% in wages paid to employees. Specifically:

What if I bring back employees or restore wages?

Reductions in employment or wages that occur during the period beginning on February 15, 2020, and ending 30 days after enactment of the CARES Act, (as compared to February 15, 2020) shall not reduce the amount of loan forgiveness IF by June 30, 2020 the borrower eliminates the reduction in employees or reduction in wages.